How debt affects mental health? | Which debt to pay off first

I came across something this week which gave me a new perspective on money. And I started to think deeply about how debt affects mental health, especially in men. After reading about someone’s tragic suicide and in honour of Debt Awareness Week – I’ve decided to write this post. All my posts are usually focussed on investing money and the power of compounding. Seldom did I think about how compound interest can equally be powerful in allowing debt to spiral out of control. Debt Awareness Week 2021 is all about destigmatising debt. Not being able to talk about this can leave us in a very dark place.

*trigger warning*

This is exactly what happened to Phillip Herron. Phillip, a single father of 3 children took his own life at an age of 34. Scrolling through Facebook, I came across this post about him from Suicide Prevention Bristol page. (full link with the image below).

Struggling with debt of more than £20k and universal credit weeks away, he could no longer hold on. When he died, he only had £4.61 in his bank account. And I could not hold back my tears as I read the note he left behind. Mental health issues are real. Social disadvantage and money related issues are one of the top factors behind this. And men are most impacted by this as research highlights that men are less likely to talk about their mental health issues.

In this post, I will cover: different types of debt, which debt to pay off first and how debt affects mental health.

Debts and their types

Debts are money that is borrowed. We borrow money all the time, whether it is to pay for a mortgage or starting a business. While not all debts are bad, some are simply the worst. For example, mortgage debts are one of best types of debt you can have. With interest rates at an all time low, taking out a mortgage can help people get on the property ladder. Yes, you do have to pay interest on your mortgage, however at the same time you benefit from two things: (a) a place to live; and (b) own a “growth asset” which can be a great long-term investment as property prices typical increases over time.

There are other types of debt such as bank loans, car loans and of course, most popular, credit card loans and overdrafts. Some of these debt comes with eyewatering interest costs which can easily spiral out of control.

How debt can grow rapidly

Borrowing money is not free. The price of borrowed money is known as the “interest rate”. Debts can start to grow rapidly due to high level of interest rates that are not paid back on time. Organisations such as banks that lend people money are doing so because they want to make money themselves. This is how retail banks make profit. Banks make profit by charging borrowers high interest while paying savers low interests on their deposits. It is easy to notice that when the Bank of England cuts their base interest rate, retail banks jump to lower their rates on the savings account, but hardly moves a dial when it comes to reducing it from their borrowers.

Therefore, compound interest is a blessing to the investors and a curse to the borrowers. [read about compound interest here]. Debts can grow rapidly out of control because missed interest costs are compounded, usually at a higher frequency than just annually.

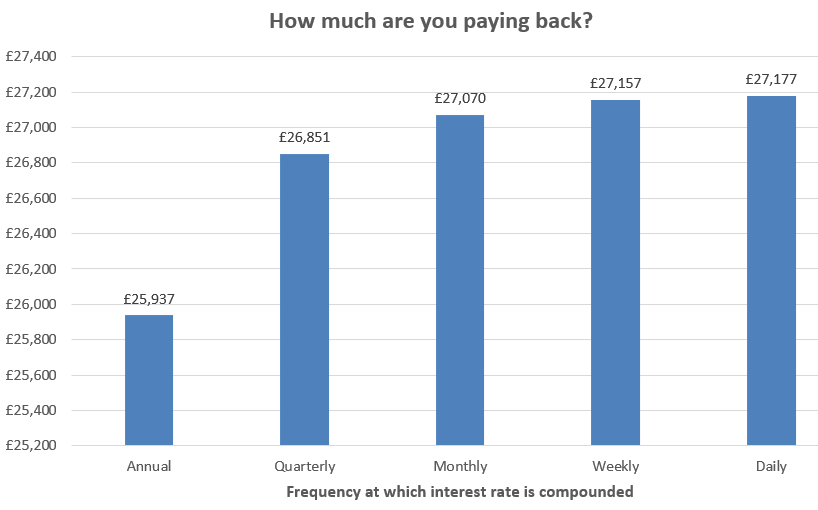

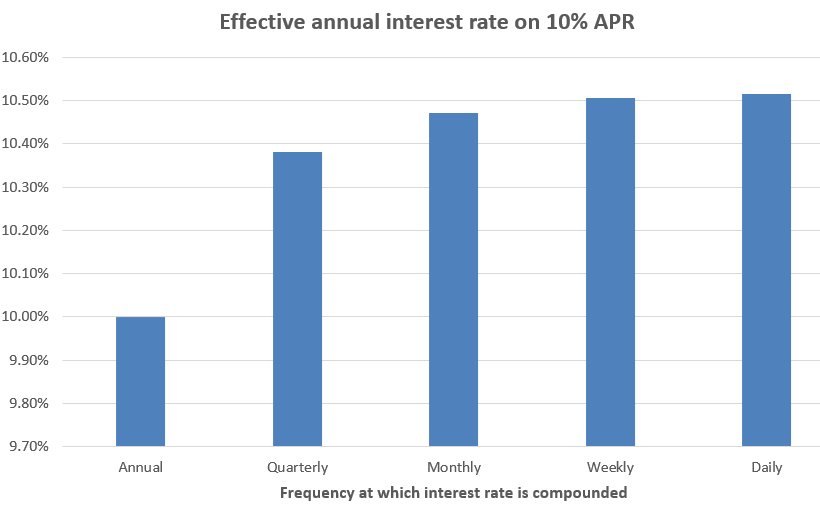

Practical example

You borrowed £10,000 over 10 years with quoted APR (annual percent rate) of 10%. The chart below shows how much you are effectively paying back on the initial £10k if the bank is compounding interest at different frequencies. As you can see, the more times the bank compounds interest, the more you are having to pay. If the bank gave you a loan at 10% APR, but are compounding it monthly then you are paying back £27,070 instead of £25,937 (if it was compounded annually) – so effectively they are charging you 10.47% and not 10%! (see the 2nd chart below)

Think of the worst case scenario where you are unable to keep up payments as expected by your bank. In that unfortunate case, the bank will then end up charging you even more than you had initially anticipated. This is because they will start charging you interest cost on the amount of interest cost that you have not paid so far (interest on interest).

This is precisely how debts can easily spiral out of control: (a) higher frequency of compounding on interest rate and (b) missed scheduled payments. Therefore frequency of compounding is a key measure to look at when thinking about which debt to pay off first.

Which debt to pay off first and how?

There are two common debt payment strategies: Debt Avalanche and Debt snowball.

Debt avalanche: you aim to pay extra money towards the debt with the highest interest rate. You start by paying the minimum amount on all your outstanding debts, then use the left-over money to pay extra towards the debt with the highest interest cost. This method will ultimately make you pay the least amount of interest cost overall and get you out of debt quicker.

Debt snowball: you pay extra on the debt with smallest monetary value first, while paying minimum on the rest. The idea is to work your way into a snowball before moving on to tackling the bigger debt. It works better with people who needs constant motivation to see that they are making some progress. However, this method will ultimately cost you more money and time as it is not technically efficient. Dave Ramsey, a renowned financial expert has said “what I have learned is that personal finance is 20% head knowledge and 80% behaviour. You need some quick wins to stay pumped enough to get out of debt completely.” – which is why he recommends this method.

You should go with the method that works best for you. Technically, it makes more sense to start paying off the debt that has highest interest cost. Generally, high interest loans tend to be short term. Therefore, interest rates on any overdrafts are likely to be much higher than a pre-agreed loan that was taken out from a bank. This is because overdrafts happen when someone draws out more money from their bank account than they own. Since this is a flexible system offered by the banks, they can essentially charge you however much they wish. They do this to deter people from using this facility too frequently. Banks do not want a sudden increase in money being taken out from their volt as it means they can no longer profit from using those money to lend out to other borrowers. Did you know that the average overdraft interest rate in august 2020 was 31.8%! (when our base interest rate was nearly 0% !!!)

Check List

Personally I would look out for the following when prioritizing on debt payments (consistent with the Debt Avalanche method):

- Loan term: shorter ones are generally more expensive. Focus on paying down the short term loans first

- APR – Annual Percentage Rate: higher the rate more expensive it is. Focus on paying down loans with higher APR

- Frequency of compound interest: Higher the frequency more expensive it is. Focus on paying down loan with higher compound frequency

- Check if there are any additional charges for late payments? Prioritise paying down those with additional penalties

- Is the debt or loan secured by an underlying asset? such as your home? It may be better to prioritise payments loans where you are at risk of repossession or losing a very valuable asset.

3 ways to reduce debt

Consolidate all your debts

This is basically taking out one big loan to pay off all the underlying smaller ones so that it becomes much easier to handle and keep up with. But be careful with who you trust to do debt consolidation with as they might end up offering you an even higher fees or have hidden policies.

A good place to start would be to visit StepChange, a charity organisation offering free debt advice.

Renegotiate current loan

Re-mortgaging are best examples of this. If you had taken out a loan couple of years ago, the chances are you are paying a much higher interest cost on them than if you were to apply now. This is because interest rates have fallen steadily over the years. There is no harm in contacting the organisation you have taken out a loan with to see if they are happy to give you a new policy term.

Get side job/side hustle

This could be a practical step. After consolidating how much you exactly need to pay every month to pay off the loan, you could take on a weekend job to earn some extra cash. The money can go towards those payments. The current national minimum wage in the UK is £8.72 for adults in the UK. If you work 14 hours a week on that payment, you could be earning nearly £500 a month (before tax). This is a healthy amount to pay towards any high interest cost loan. It is of courser easier said than done. But, sometimes to take a jump you first have to take a few steps back. And jumping over the initial hurdle requires short term commitment and consistency.

How debt affects mental health

In every way possible. At the beginning of the blog, I wrote about Phillip’s journey. Debts can give a horrible feeling that can linger on back of our minds regardless of what we are doing. It can eat away sleep and prevent us from having a wholehearted laugh. It can affect one’s mental health which may not be always visible. Here’s how:

Obligation

It’s a contractual obligation that can penalise us for not being able to fulfil. And so, thinking of its consequences is always dire.

You see it balloon up

When things are not going to plan and you have trouble keeping up with payments, the debt amount can shoot up quite aggressively. It may feel hopeless when you don’t see the light at the end of the tunnel. But when it feels too much, never hesitate to ask for help. Check out charities like mind.org.uk and mentalhealth.org.uk

You feel ashamed to talk about it

Taking out a loan out of necessity is not something one feels comfortable talking about. It may feel embarrassing to discuss this with friends and family. However, at the end of the day someone from your social circle could be that helping hand you need. You just never know where and how help can get to you.

You feel there is a lot at stake and a lot to lose

Feeling stuck is a human thing. When everything gets too much, take a break, and restart your thought process from scratch. Make a spreadsheet listing all the loans you need to pay back and decide on which debt to pay off first. It could be that, by focusing on a high cost loan first gives you some breathing space to tackle the rest. Don’t let debt affect your mental health

The summary

- Everyone has some form of debt tucked away in their finances, whether it is a student loan, a mortgage or a loan from the bank. You are not the only one.

- Try your best to keep up with debt payments, don’t let it get out of control. Prioritise keeping with your debt payments over saving or investing money. Debt can balloon up aggressively due to compound interest.

- If it does feel out of control, seek help (both for your mind and finances) and start to prioritise which debt to pay off first.

- Debt affects mental health. Look after your health and seek help, don’t suffer alone. There is no shame in sharing how you feel. This goes especially to men. And if you are one of the lucky ones to not have to worry about debt, then look around – there is someone you know who might need a friendly hand.

Read these great posts from other bloggers from the UK Money Blogger community:

- Let’s talk about debt – MrsMummyPenny

- How to pay off debt faster – Miss Many Pennies

- Become debt free – 5 things to do now – Bee Money Savvyy

- 8 Best ways to pay off debt – Money Savvy Mum UK

- 5 Amazing Debt Charities That Give Free Debt Advice – Cash Back Collette

- 10 steps to get out of debt – Broke in Bristol

- LETS TALK ABOUT DEBT – The Reverend

- Embrace frugal living to pay off debt – Shoestring Cottage

- How to get out of debt on a low income – Great Deals Made Easy

- Drowning In Debt? 9 Ways To Build Yourself A Life Raft – Young Fun and Thrifty

You may wish to check out some great content from other UK Money Blogger’s pages from Feedspot: UK Personal Finance and UK Investment Blogs