Stock Market Crash : Risk & Opportunities for investors (during COVID-19)

Stock Market Crashes are natural part of a business cycle. They may have different triggers but expecting them should not be unexpected. Market practisioners have been discussing this for some time now as its been over a decade that the last recession had hit. This time around, its not driven by bad loans in the financial markets but by the deadly health pandemic. Unfortunate trigger but the aftermath in the financial market is not totally unprecedented. Here’s what you need to understand about how the current financial market behaviour and how it is creating opportunities for long term investors. Let’s discuss this with a risk hat ON.

Arrival of the “Black Swan” (Investment Risk)

Nassim Nicholas Taleb in his book ‘The Black Swan’ (Taleb, 2007) defines such event with 3 main characteristics:

- an outlier beyond the normal range of expectations;

- has a huge impact;

- despite #1, we create explanations for it in hindsight, making it seem “explainable and predictable.”

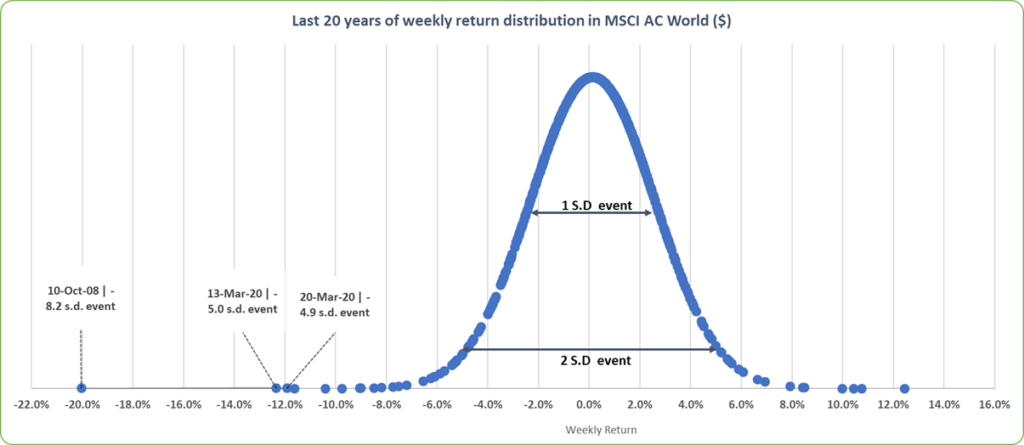

By these definitions, we can classify the current COVID-19 pandemic as a “Black Swan” event. Let’s put this statistically. As a proxy of equity market returns, the chart below draws upon statisticians’ favourite, a normal distribution. The bell-shaped curve is showing weekly market returns of MSCI AC World ($) over last 20 years. According to law of large numbers, weekly return of this equity market index is expected to be between approximately +/-2.5%, 68% of the times. Graph also shows that COVID-19 market crash has placed recent market returns within an extreme left tail territory (well beyond normal range of expectations). The -12.3% weekly return on 13th March 2020 corresponds to a 5 standard deviation event. As a reference point, the worst weekly return observed during GFC was a 8 standard deviation event. No doubt we are navigating through a regime of extreme volatility.

Volatility creates (investment) opportunity

Investing through this climate of heightened volatility, one of the most difficult problems likely to be faced by investors is time blindness. It is the inability to assign a duration to the passage of this volatility. Nevertheless, it is equally important to remember that on the other side of volatility lies opportunity. Volatility does not equate to risk. High volatility could also be a powerful catalyst for active decision making as wild swings work both ways.

Return dispersion and pairwise correlation of stocks helps to quantify the current level of opportunity present in the market. Dispersion is a measure of magnitude of return differences between stocks. Average pairwise correlation is the level of co-movement within a group of stocks. During times of crisis, heightened volatility is reflected in both high dispersion and correlation figures. An increased level of correlation reduces the benefits of diversification and makes a convincing case for high conviction stock pickers. Likewise a higher level of dispersion, caused by larger differences between winners and losers, offers a solid foundation for active managers to utilise their stock picking skills. These numbers across many market indices have recently peaked highlighting that its a good time to invest in a good active fund.

…behavioural risks is higher during stock market crash

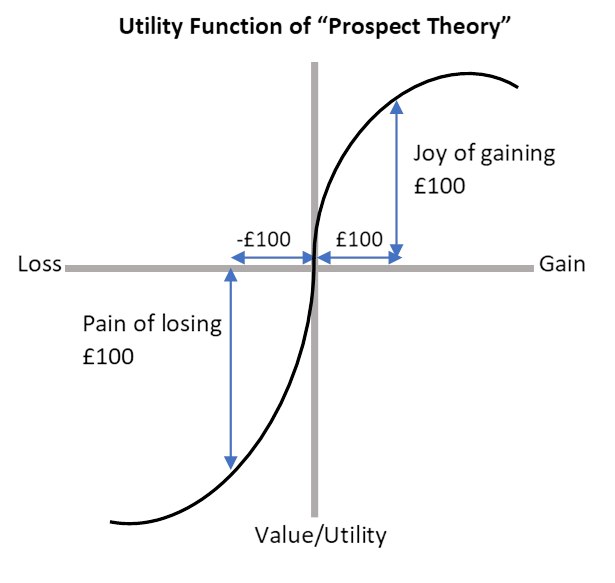

“In human decision-making, losses loom larger than gains.” (Kahneman & Tversky, 1979)

Development of Prospect Theory and its succeeding work by Daniel Kahneman and Amos Tversky in 1979; earned Kahneman Nobel Memorial prize in 2002 and Tversky in 2017. Studies in behavioural finance have highlighted a number of cognitive & emotional biases which could be rooted in decision making.

Loss Aversion

Did you know that the feeling of pain due to a loss could be 2-2.5 times greater than the feeling of pleasure from an equivalent gain? (Kahneman & Tversky, 1979), see chart above. Loss aversion could lead you to hold onto losers for too long or sell out of winners too quickly.

Status Quo

Another implication of loss aversion is that individuals have a strong tendency to remain at the status quo over a better option. Research by Brown and Kagel identified two tendencies which produces status quo in investors: i) choosing not to compare returns on the current stock holding relative to available alternatives and (ii) choosing to hold onto suboptimal stock after comparing returns with other stock alternatives (Brown, 2009). Another study also found that status quo was particularly higher during negative emotional climate(Li, 2009). Now is a good time to compare & revisit your stock investments.

Mental Accounting & Anchoring

These biases impact us as we process new information. In mental accounting, investors treat assets as less fungible than they really are. A typical example could be looking at groups of stock by specific buckets without estimating correlations between the buckets. For example, expecting a group of “technology” stocks to outperform another group of “value” stocks may not materialise during a heightened crisis period. This is because traditional correlations between the buckets may no longer hold true.

Likewise with anchoring, individuals imprints the first information received as a reference point. This is even after receiving subsequent information which could be more relevant and/or realistic. Empirical studies found that if a stock price drops, an investor may wait to break-even before selling despite other indicators suggesting that a recovery in price is unlikely (Campbell, 2009). Have one of your stocks lost its way during this stock market crash, and unlikely to recover? Check!

The summary

- Recessions are inevitable; and Black Swan events do occur

- Understanding concepts of investment risk is key to quatifying whether a market-sell off is truly unprecedented or not

- Volatility rises during times of crisis but it also creates opportunities for long term investors as prices swing both ways (Read post on investing through stock market crash)

- While investing during stock market crash, its important to touch-base with one’s inherent behavioural biases (we all have them!)